Sustainability Management

Materiality Analysis

USI annually conducts a materiality analysis using the GRI Standards, AA1000 Stakeholder Engagement Standards, and the AA1000 Accountability Principles of Inclusivity, Materiality, Responsiveness, and Impact as our framework to identify material issues for ESG disclosure. The assessment is conducted based on the Double Materiality principle referenced from GRI 3: Material Topics 2021 and the ESRS within the EU CSRD framework. To evaluate and rank the significance of sustainable issues across economic, environment, and people/human rights dimensions, we integrate the Value Balancing Alliance (VBA) methodology, Harvard Business School Impact-Weighted Accounts methodology, London Benchmarking Group (LBG) framework, and TIMM Impact Evaluation framework. The results are then prioritized and ranked according to their significance, presented to the Sustainability Committee, and incorporated into our enterprise risk management process to serve as a reference for setting our long-term sustainability goals and strategies. This materiality assessment process, content, and data are independently verified by a third-party assurance provider.

The 15 material issues defined in 2024, and its 2029 long-term targets are part of executive senior managers' performance scorecard, such as key talent retention and local procurement rate. GHG emissions are linked to executive senior managers' (including the CEO) compensation as part of our climate strategy to link our operational goals with sustainable goals.

Phase I. Inclusivity: Identify Stakeholders & Design Sustainability Surveys

In 2024, we defined our 6 major stakeholder groups as: shareholders/investors/banks, employees, customers, suppliers/contractors, governments/industry unions/associations, and communities (including NGOs and the media).

We integrated the SDGs, GRI Standards, SASB Standards, TCFD and TNFD frameworks, RBA Code of Conduct, S&P Global CSA indicators, and MSCI ESG Rating indicators with our industry specific characteristics and ASEH's requirements and compiled them into 9 governance issues, 7 environmental issues, and 6 social issues, 22 sustainable issues in total.

Phase II. Materiality: Investigate Stakeholder Concerns & Double Materiality Impact Analysis

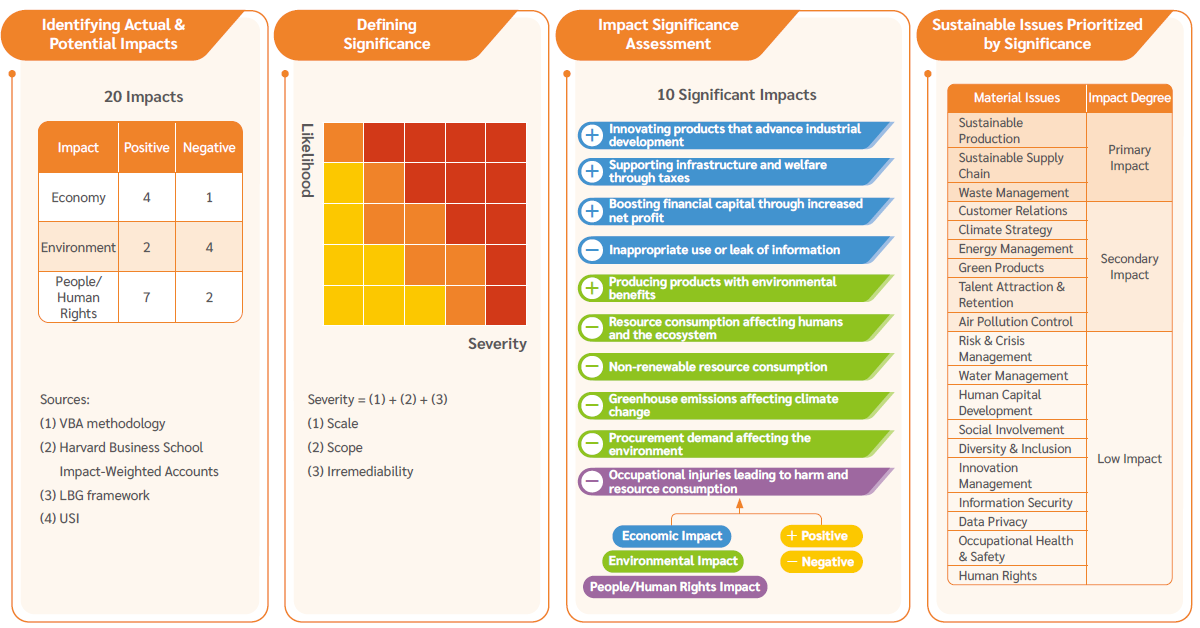

In 2024, we collected 1,216 Stakeholder Concern Surveys from external and internal stakeholders and identified issues of high stakeholder concern.

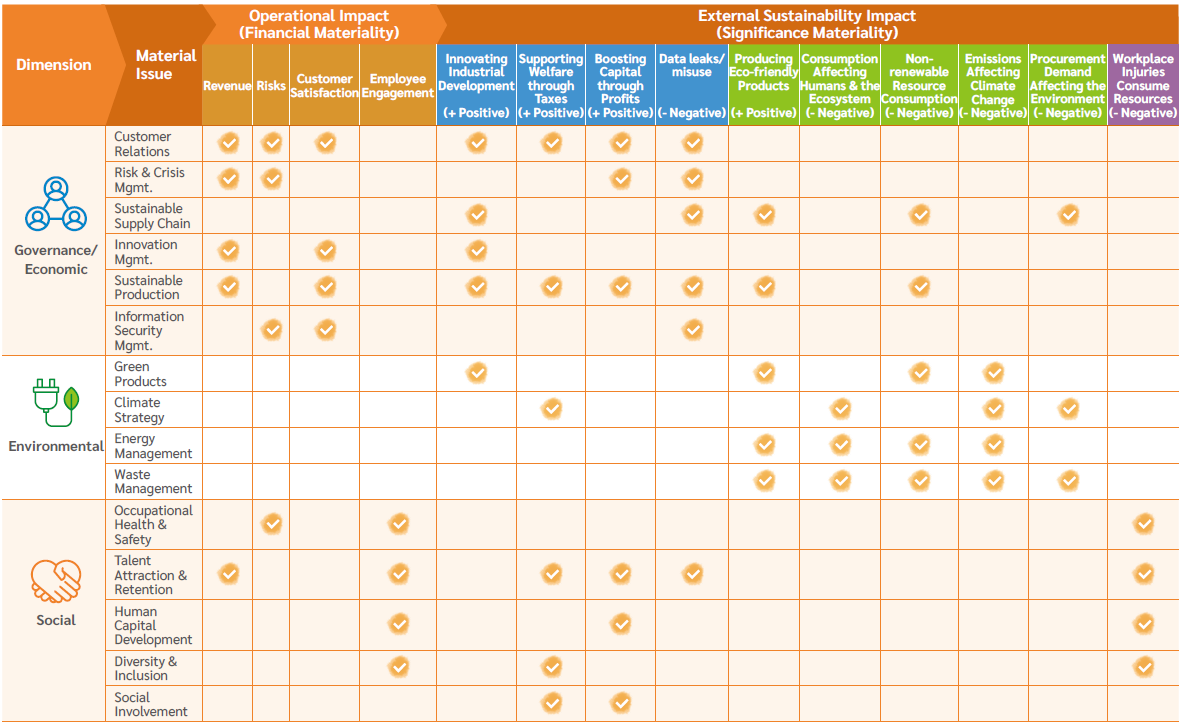

Using the EU concept of double materiality, we conducted an Operational Impact Survey to reflect Financial Materiality by measuring the impact of each sustainable issue on the Company's revenue, risks, customer satisfaction, and employee engagement. 94 senior executives and Sustainability Committee members filled out this survey as representatives of USI's operations.

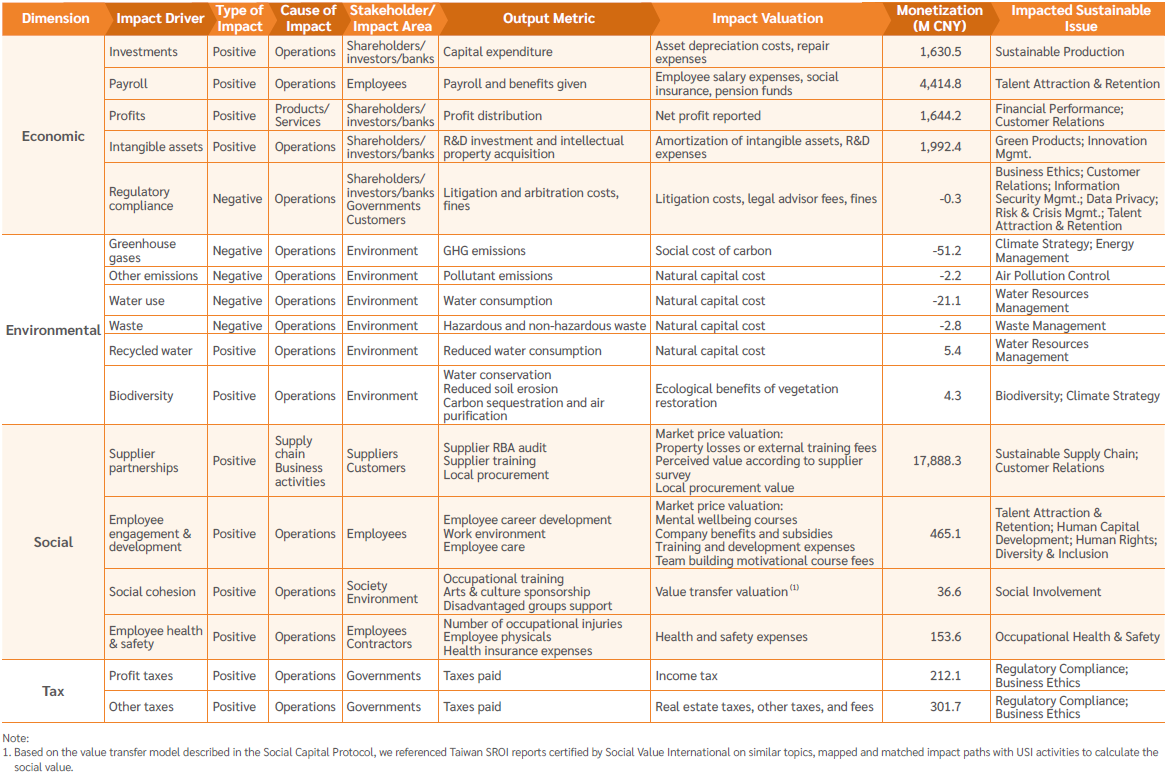

To quantify Significance Materiality, apart from incorporating TIMM impact evaluation results, 56 managers and colleagues conducted an External Sustainability Impact Survey that includes 13 positive impacts and 7 negative impacts on the economy, environment, people/human rights and assesses the severity and likelihood of actual and potential impacts. The survey results identify 10 significant impacts, including 3 positive and 1 negative economic impacts, 1 positive and 4 negative environmental impacts, and 1 negative social impact.

Impact Evaluation-External Sustainability Significance Impact

Double Materiality Results Matrix

Phase III. Responsiveness: Identify Material Issues & Define Topic Disclosures and Boundaries

We assessed the significance of the issues by cross analyzing the Stakeholder Concern Survey, Operational Impact Survey, and External Sustainability Impact Survey, then mapped it to previous material issues and consulted external experts and the Sustainability Committee to determine 15 material issues. The materiality assessment results were then reviewed and approved by the Board of Directors.

We mapped 14 GRI topic standards and 8 USI specific topics that respond to the material issues identified. Non-material issues are also disclosed in this report as they are essential in USI's sustainable development.

Following the principle of comparability, our 2024 Sustainability Report covers the material issues of the previous year. The structure of this report follows indicator reporting requirements and fully discloses USI's current policies and plans for fulfilling ESG sustainability development.

Phase IV. Impact: Formulate Long-term Goals & Evaluate Impact

As part of our analysis, we identify the material risks and opportunities of our material issues for long-term value creation. To mitigate negative impacts and manage these issues, USI's five Sustainability Taskforces have disclosed management approaches and strategies for each material issue according to their requirements, formulating 41 long-term goals.

In addition to quarterly Executive Team meetings, the Sustainability Taskforces also meet semiannually to review the progress of each goal. At the annual Sustainability Committee meeting, we review our achievements, make rolling adjustments, track sustainability trends, and manage the impact of our sustainability goals. We publicly disclose the direction, progress, and performance of our sustainability goals in our annual ESG Report.